Residential real estate investing is one of the fastest ways of growing your net worth and becoming rich. This detailed article will show you how, based on a real example with real numbers. It will also talk about the first real estate deal I’ve ever done a few years ago. So I made many mistakes but learned a lot. Still grew my net worth significantly, so no regrets.

Synopsis

Here’s a brief summary of what we’ll be discussing:

- Learning real estate tips, as well as the pros and cons of common ways of making money in real estate.

- Rule of thumb for rental properties: for every $100K of real estate property cost, the rental amount should be over $500 a month; ideally $1,000. This is the 1% rule.

- Why residential real estate is one of the best forms of wealth building. How I got started.

- In-depth example of a residential real estate property with a net worth increase of 20-30% a year.

- Calculation of net operating income (NOI), capitalization rate, cash flow, net worth increase, return on investment (ROI) and return on equity (ROE).

- Access to the Rental Real Estate Investment Model I’ve built in Google Sheets, which you could use for your own real estate analysis and view all the calculations and charts.

- Risks of investing in residential real estate, including market crashes, high leverage, vacancy, interest rate increases, and other risks.

Below we’ll look at what I consider one of the best ways of real estate investing for beginners, which is residential rental properties.

Calculating a Good Residential Rental Property Investment

The rental properties I own now are some of the best investments I ever made. I invested in some REIT ETFs as well, but buying physical homes brought me far greater returns. Let’s dive in.

There’s a simple rule of thumb that I follow: for every $100K of real estate property cost, the rental amount should be at least $500 a month, ideally $1,000. If it does indeed reach $1,000 per $100K, this is what is known in the industry as the 1% rule. These properties are not easy to come by.

For example, a property worth $400,000 should rent out for at least $500 x ($400K/$100K) = $2,000 a month plus the utility costs (i.e. Tenants should pay for heating, water, electricity, phone, cable, and internet). In this case, you generally won’t be making much or any cash flow but you might break even. It would be better if the property rents for more, at $4,000 per month, so that it qualifies for the 1% rule and brings in positive cash flow.

One disadvantage is that this form of investing requires huge sums of capital to get started. Not everyone has a 20%, or even a 5%, down payment readily available to buy a $400,000 house; that’s an $80,000 down payment plus closing costs. Closing costs can range from $5,000 to $20,000 on such a property, depending on the location and your situation.

However, if you’re able to get a mortgage and have the required capital, this form of investing is one of the best. Not only do you have the potential to have positive cash flow from such investments every month, but the capital appreciation and mortgage payoff benefits are huge in the long run.

Residential Rental Real Estate Property Example with Calculations

Let’s look at some calculations of an actual example from my own real estate investing experience. We’ll walk through free cash flow, net operating income, capitalization rate, net worth increase, return on investment and return on equity.

I’m rounding some of the numbers for simplicity:

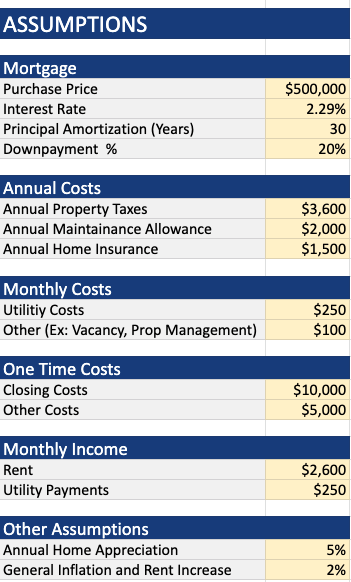

- I bought a semi-detached house in Brampton, Ontario, Canada for $500,000.

- I had to save for the down payment of 20%, which was 20% x $500,000 = $100,000.

- Mortgage amount: $400,000 at a very low-interest rate of 2.29%, a 5-year term and a 30-year amortization period.

- The closing costs were $10,000 since I had certain benefits because I was a first time home buyer.

- Initial renovations were $5,000 to get the property into a decent rentable state.

- You’ll see some other details in this Rental Real Estate Investment Model.

Calculating Monthly Free Cash Flow

We’ll start with something really simple; monthly free cash flow. This is basically the amount of money I got coming in (inflows) every month minus the amount that was leaving (outflows). Below are the inflows and outflows for this example.

Monthly Avg. Cash Outflow

- Mortgage payment: $1,531.

- Property tax: $300.

- Utilities: $250.

- Avg. maintenance allowance: $167.

- Home insurance: $125.

- Vacancy allowance: $100.

- TOTAL MONTHLY CASH OUTFLOW: $2,473.

Monthly Avg. Cash Inflow

- Rent: $2,600.

- Utilities: $250.

- TOTAL MONTHLY CASH INFLOW: $2,850.

Monthly Free Cash Flow

- Monthly Free Cash Flow = Monthly Cash Inflow – Monthly Cash Outflow

- Monthly Free Cash Flow = $2,850 – $2,485

- Monthly Free Cash Flow = $377

Some investors also add a property management expense, which ranges from 8-12% of the rental amount. In my case, I managed the property myself. Therefore, the total monthly cash flow I roughly generated from this property was $377. On a yearly basis that turned out to be just over $4,000. But I’ll provide more details on annual figures in the yearly calculation below.

Calculating Yearly Free Cash Flow

This is the same thing as the monthly cash flow but on an annual basis.

Annual Avg. Cash Outflow

- Mortgage payment: $18,375.

- Property tax: $3,600.

- Utilities: $3,000.

- Avg. maintenance allowance: $2,000.

- Home insurance: $1,500.

- Vacancy allowance: $1,200.

- TOTAL ANNUAL CASH OUTFLOW: $29,675.

Annual Avg. Cash Inflow

- Rent: $31,200.

- Utilities: $3,000.

- TOTAL MONTHLY CASH INFLOW: $34,200.

Annual Free Cash Flow

- Annual Free Cash Flow = Annual Cash Inflow – Annual Cash Outflow

- Annual Free Cash Flow = $34,200 – $29,675

- Annual Free Cash Flow = $4,525

Some investors will consider expenses such as closing costs and renovations in their first year cash flow numbers as well. In this case, the first year cash flow will be lower than the subsequent ones. Others will consider those initial expenses as the initial investment with the downpayment. Above, we kept it simple though and didn’t include those numbers in the cash flow calculation.

If we were to consider those initial cash outflows, here is what the numbers would look like year after year:

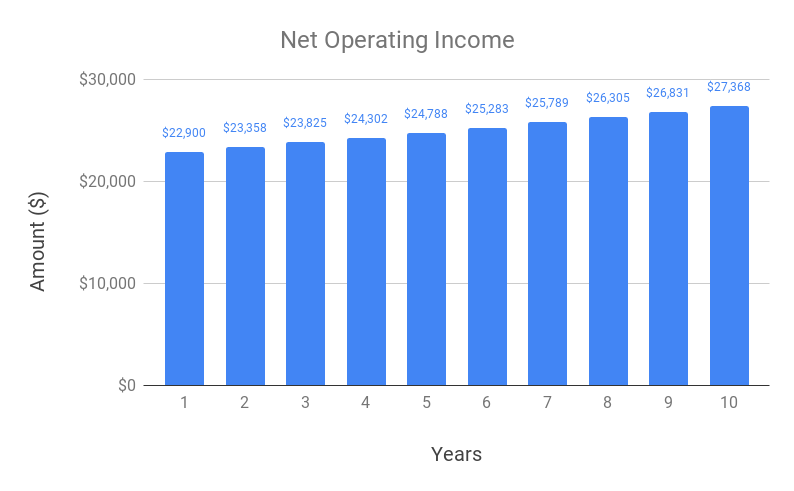

Calculating Net Operating Income (NOI)

The Net Operating Income (NOI) is calculated as total income minus all expenses, not including the borrowing costs (i.e. mortgage payments). In our example the first year NOI is:

- NOI = Total Income – Total Expenses

- NOI = $34,200 – ($3,600 + $3,000 + $2,000 + $1,500 + $1,200)

- NOI = $34,200 – $11,300

- NOI = $22,900

You can see the next 10 years’ NOI amounts in this chart:

It’s getting a bit more advanced, but you’ll get it after looking into the calculation details on the Rental Real Estate Investment Model. It’s a real estate investment calculator I built that allows you to input all the different variables and make assumptions. After which the model would automate all the calculations.

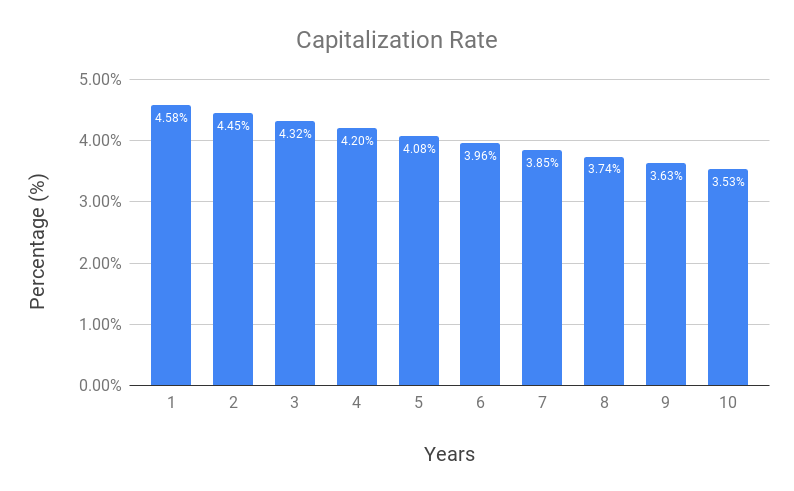

Calculating Capitalization (Cap) Rate

The capitalization rate or cap rate is the ratio of NOI to the total asset or property value. It’s calculated by dividing annual NOI by the property asset value. It can fluctuate every year depending on if the NOI or the property value changes.

The first year cap rate on the example above can be calculated as follows:

- Cap Rate = NOI / Property Value

- Cap Rate = $22,900 / $500,000

- Cap Rate = 4.58%

It’s a useful metric to help investors determine how attractive a certain investment is. The idea is that if you wouldn’t have any debt on the property, how much income can you generate relative to your deployed capital? Generally, a cap rate of over 5% is decent. If you can get 8% or higher, that’s considered really good in residential real estate. In my example, I got slightly below 5%, which is not great. But at the time when I bought the property, I was still happy with it because the GTA market was on fire and I really wanted to get into the market and invest in my first investment property.

The cap rate tends to decrease over time if the property value keeps increasing in price faster than your net operating income (NOI). In the model assumptions, the fields that affect this are called the “Annual Home Appreciation” and “General Inflation and Rent Increase”. Because the assumption was made that property value increases 5% year-over-year, while rents only 2% per year, the cap rate decreased over time. Below is the chart of the cap rate in our example over time:

Net Worth Increase or Total Return Calculation

The net worth increase is slightly more complicated and requires more assumptions. Some investors refer to it as your total return. Sometimes the total return is used to mean several things and is used interchangeably with net income, which can cause confusion. I choose net worth increase as the name because it’s more descriptive. This is my “go-to” metric when analyzing real estate deals. Increasing my net worth is the reason why I like investing, so naturally, this calculation is crucial. In its calculation, we combine all numbers in the deal.

There are four main elements to net worth increase or total return when it comes to residential real estate. These include:

- Cash Inflow

- Cash Outflow

- Principal Paydown

- Property Value Increase

In our example, for the first year, here are the numbers:

- Cash Inflow = $34,200

- Cash Outflow = $29,675 + $10,000 + $5,000 = $44,675

- 1st year Principal Paydown = $9,215

- Assumed Property Value Increase = $500,000 x (1+ 0.05) – $500,000 = $25,000

The assumption is that the property increased by 5% year over year (YoY). Another assumption we didn’t cover in the cash outflow calculation before are the closing costs of $10,000 and the $5,000 initial renovation costs.

The calculation for the first year net worth increase or total return for this residential real estate investment is as follows:

- Net Worth Increase (Total Return) = Cash Inflow – Cash Outflow + Principal Paydown + Property Value Increase

- Net Worth Increase (Total Return) = $34,200 – $44,675 + $9,215 + $25,000

- Net Worth Increase (Total Return) = $23,740

Another way this can be calculated is:

- Net Worth Increase (Total Return) = NOI + Property Value Increase + Principal Paydown – Mortgage Payment – Expenses Not in NOI Including Closing and Renovation

- Net Worth Increase (Total Return) = $22,900 + $9,215 + $25,000 – $18,375 – $15,000

- Net Worth Increase (Total Return) = $23,740

This could have been simplified further because the Mortgage Payment minus the Principal Paydown equals Mortgage Interest:

- Net Worth Increase (Total Return) = NOI + Property Value Increase – Mortgage Interest – Expenses Not in NOI Including Closing and Renovation

- Net Worth Increase (Total Return) = $22,900 + $25,000 – $9,160 – $15,000

- Net Worth Increase (Total Return) = $23,740

All approaches give the same result. I prefer the first method since it’s simpler and is easier to visualize. Again, your annual net worth increase will fluctuate every year, but will likely be higher every year.

The second-year Net Worth Increase (Total Return) equals $40,659. The third year equals $42,655.

Cumulatively after 3 years for this example, according to the assumptions and the model, the net worth increase is $107,054. Below you’ll see the net worth increase over 10 years:

Calculating Return on Investment (ROI)

Return on investment (ROI) is simply your annual net worth increase relative to your initial investment. The first year ROI calculation for our purposes can be seen as:

- Annual ROI = Annual Net Worth Increase / Initial Investment

- Annual ROI = $23,740 / $100,000

- Annual ROI = 23.74%

To calculate the second year ROI, the denominator stays the same at $100,000 because this is your initial cash investment. But this time we consider the second year annual net worth increase:

- Annual ROI Year 2 = Annual Net Worth Increase Year 2 / Initial Investment

- Annual ROI Year 2 = $40,659 / $100,000

- Annual ROI Year 2 = 40.66%

To get the cumulative ROI, just add all the net worth increases up until the period for which you are calculating it. For example, the cumulative ROI after the second year equals 64.40%:

- Cumulative ROI Year 2 = (Annual Net Worth Increase Year 1 + Annual Net Worth Increase Year 2) / Initial Investment

- Cumulative ROI Year 2 = ($23,740 + $40,659) / $100,000

- Cumulative ROI Year 2 = 64.40%

Below is the ROI for the first 10 years:

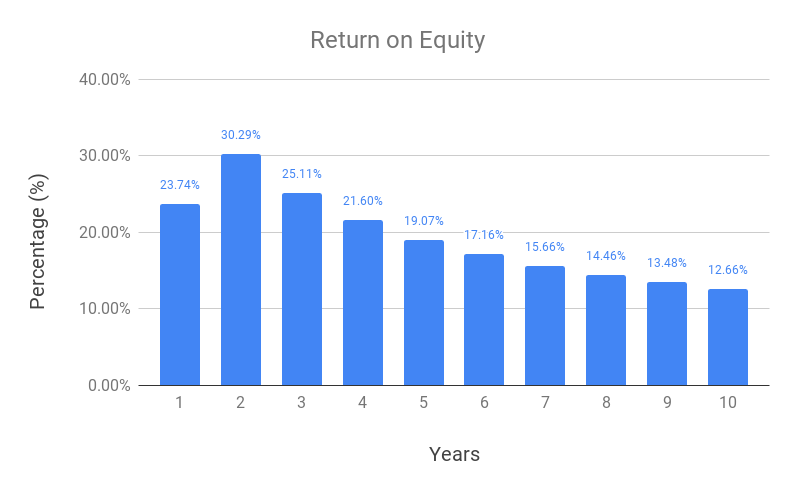

Calculating Return on Equity (ROE)

Return on equity (ROE) is basically your return or net worth increase (income, debt paydown, and capital appreciation) divided by equity (the amount of equity in your investment). Return can be interpreted in a couple of ways. I consider it as the amount equal to your annual net worth increase. Some investors may refer to ROE as cash-on-cash return with equity.

Please note, a lot of investors confuse Return on Investment (ROI) and Return on Equity (ROE). The difference is simple, the denominator for ROI remains your initial investment capital. Whereas, for ROE the denominator is the equity portion in the deal at any given point, which changes over time. As such, here’s the calculation for the first year:

- Return on Equity (ROE) = Annual Net Worth Increase / Equity

- Return on Equity (ROE) = $23,740 / $100,000

- Return on Equity (ROE) = 23.74%

Notice how ROE and ROI are equal in the first year. That’s because, in our assumptions, the initial investment equals the equity at the beginning of the first year. The second-year ROE equals 30.29%:

- Return on Equity (ROE) Year 2 = (Cumulative Net Worth Increase Year 2) / Equity in Home

- Return on Equity (ROE) Year 2 = $40,659 / $134,215

- Return on Equity (ROE) Year 2 = 30.29%

The third-year ROE equals 25.11%:

- Return on Equity (ROE) Year 3 = (Cumulative Net Worth Increase Year 3) / Equity in Home

- Return on Equity (ROE) Year 3 = $40,659 / $134,215

- Return on Equity (ROE) Year 3 = 25.11%

ROE can help you determine when it’s worth pulling some of your equity out of a property, as the number generally decreases over time. To help you determine that, you need to think about what kind of ROE you’d like to earn on your capital.

For example, if your target return is 15%, then you might want to consider refinancing, selling or having another exit strategy to pull out your equity when the ROE falls below that threshold. In our example, that looks like year 8 is when we should think about pulling out at least some of the equity. That’s because the ROE becomes 14.46% and continues to fall in the following years. You can then redeploy that pulled capital into other investments that can generate over your target return of 15%.

Risks of Investing in Residential Rental Real Estate Properties

- Real estate prices are subject to market crashes and price drops. Losing a huge chunk of your capital is not as uncommon as you may think. During financial recessions a lot of people are unable to afford houses, therefore demand for real estate falls. When that happens, house prices fall.

- There’s the potential of losing more than your initial investment. This is due to leverage since it’s a double edge sword. On one hand, when you borrow money to invest in real estate, during good years your returns multiply by your leverage factor. But on the other hand, during bad years when real estate prices drop, your losses multiply by your leverage factor. For example, if you borrow 80% of your real estate value, your leverage factor is 5x, calculated as 100/(100-80) = 5. Which means your returns magnify by 5 times.

- Rising interest rates affect how much your mortgage payment will be. This is because your interest expense on the loan amount increases the higher the mortgage interest rate is. Therefore, when interest rates are high or are rising, your profit takes a hit. Higher interest rates could also mean that you are less likely to qualify for a new mortgage or a renewal on your existing mortgage.

- The vacancy of a rental property can greatly affect real estate investment profitability. If your real estate property is sitting there vacant with no tenants it is generating negative cash flow. The goal of every real estate investor is to make sure the vacancy is as close to 0% as possible. At the same time, you don’t want to rent your rental property to just anyone. This brings us to the next point.

- Troubled tenants can be a really big issue. If you don’t pick your tenants properly with a strict checklist you may end up with tenants that are causing trouble, do not pay rent, destroy your property, disturb others in the area, or cause other problems. Evicting tenants can cost quite a bit and takes months. At least, this is the case in Canada. Specifically, I had to evict tenants in Ontario. There are only a handful of reasons why you can kick tenants out. The process needs to be followed strictly, otherwise, your case will be dismissed by the Landlord & Tenant Board.

- Real estate taxes – the example in the previous section assumed no income taxes on the property; only the investment property tax. You can write off many expenses while running your real estate business, so your taxable income should be minimal, but there may still be some taxes involved. Be sure to account for taxes in your personalized calculations.

- Liquidity is another disadvantage of investing in real estate. It’s much harder to buy and sell real estate compared to other assets, such as stocks, bonds, ETFs, and mutual funds. It could take several weeks or months to buy and sell real estate, whereas stocks can be bought and sold in seconds.

- In residential real estate, there will often be unexpected maintenance and repair costs. Appliances, furnaces, air conditioners, roofs, and many other things could break or malfunction and require repairs. It’s a good idea to set aside some funds from your investment every month for these kinds of unexpected costs.

- Another risk some investors may consider in unpopular locations is rental costs falling. This is highly unlikely, however, in certain remote locations where demand for housing is falling, this can be a real issue. We’ve also seen how the effects of COVID-19 affected the rental market. As vacancy increases, it becomes a tenant’s market, which puts pressure on rent prices. That’s because a lot of houses are available for rent, while the rental demand falls.

Concluding Remarks on Residential Real Estate Investing

So, is residential real estate a good investment? There are definitely a lot of risks associated with investing in real estate, just like any other investment. However, with the right type of real estate property, the benefits often outweigh the risks. Make sure to buy real estate that makes financial sense. The real estate model used in this article can be a great tool to help you analyze a potential property you’re thinking of buying.

To view the real estate model I’ve built in Google Spreadsheets, click here to download it and make your own copy. Input your own assumptions that are unique to your situation. The model does have some flaws, such as the exact mortgage payments may not match the actual amount and the debt vs. principal amounts are not exact, but very close. Many might want the closing costs to be considered as part of the initial investment, which is not what the model assumes. No model is perfect, but it should still help you distinguish between a good rental real estate investment from a bad one.